10 Expert Tips to Boost Your Home Loan Eligibility & Get Approved Fast

Admin

Admin

- 26th Feb 2025

- 1188

- 0

Never miss any update

Join our WhatsApp Channel

For most people, buying a home is a big dream - one that usually needs a home loan to turn into reality. But here's the thing: getting a loan isn't always a cakewalk. Many hopeful buyers face rejection, sometimes for reasons they never saw coming - low credit scores, too much debt, or just not ticking the right financial boxes.

Want to up your chances of approval? Then, you've got to play it smart. Banks and lenders have a set of rules they follow before handing over a loan, and understanding these ground rules can help you tweak your financial game plan.

What Lenders Look At Before Approving a Home Loan

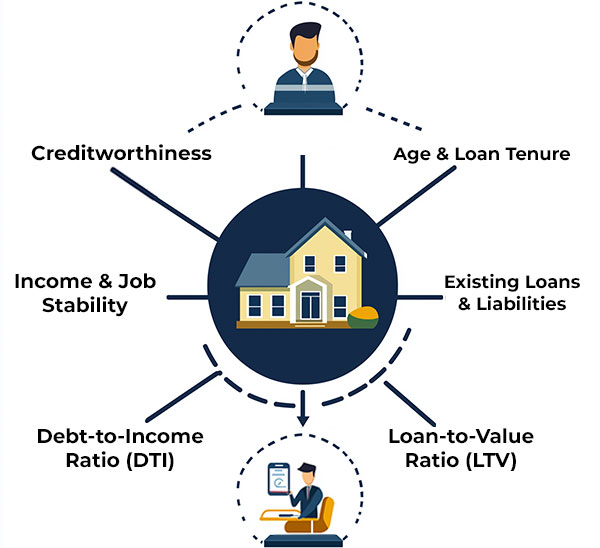

Financial institutions don't just hand out loans to anyone who applies. They weigh a bunch of factors before giving the green light. Some of the key ones include:

-

Creditworthiness - Your credit score tells the story of your financial habits. The higher, the better!

-

Income & Job Stability - Lenders love steady earners. A stable job history makes you a safer bet.

-

Debt-to-Income Ratio (DTI) - The less you owe compared to your income, the more likely you'll get approved.

-

Loan-to-Value Ratio (LTV) - The percentage of the property's cost that the bank is willing to cover.

-

Existing Loans & Liabilities - Got a bunch of active loans? That could be a red flag for lenders.

-

Age & Loan Tenure - Younger applicants with longer tenures often have an edge.

If you're serious about securing that loan, you've got to fine-tune these factors before applying. Below are 10 no-nonsense tips to get you across the finish line.

10 Ways to Improve Your Home Loan Eligibility

1. Stretch the Loan Tenure

Longer tenure means lower EMIs, which makes repayment seem less intimidating. But here’s the catch: you'll pay more interest in the long run. If you need that extra cushion to get approved, though, it's an option worth considering.

2. Pay Off Existing Debts First

Before jumping into a fresh loan, trim down your financial baggage. A lower DTI ratio signals that you've got a handle on your money. Credit card dues, personal loans - clear them up and watch your eligibility score rise.

3. Boost Your CIBIL Score

Your CIBIL score can make or break your loan chances. Here's how you can push it upwards:

-

Clear outstanding dues pronto.

-

Never miss EMIs or credit card payments.

-

Keep credit card usage below 30% of the limit.

-

Avoid applying for too many loans in a short span.

4. Increase Your Monthly Income Streams

More money coming in means you can afford a bigger loan. If you're aiming for a higher loan amount, look for additional revenue streams - freelancing, rental income, side hustles. The stronger your earnings, the better your profile looks to banks.

5. Choose Your Lender Wisely

Not all banks and lenders are created equal. Some are lenient towards self-employed folks, while others favor those with impeccable credit. Compare interest rates, processing fees, and flexibility before you commit.

6. Go Big on the Down Payment

A larger down payment (20%-30%) reduces the loan amount you need. This makes you less risky to lenders and could even land you a better interest rate.

7. Keep Your Loan-to-Value (LTV) Ratio Low

Banks love a low LTV ratio - it tells them you’ve got skin in the game. Aim for an LTV below 80%, and you'll be in a stronger position.

8. Stick to One Employer (If Possible)

Lenders dig job stability. If you're constantly hopping jobs, they might see you as a risky borrower. Ideally, try to have at least 2-3 years of steady employment before applying.

9. Don't Go on a Loan Application Spree

Every loan application sends a signal to credit bureaus, nudging your score down a bit. Apply smart - stick to one or two well-researched options instead of flooding the market with requests.

10. Consider a Joint Loan

Teaming up with your spouse for a joint loan can give your eligibility a serious boost. Banks consider both incomes, which means you might qualify for a bigger loan. Plus, you get tax perks on both principal and interest payments.

Final Thoughts

Locking in a home loan isn't just about filling out forms and hoping for the best. It's about setting up your financial profile to look rock-solid. Work on your credit score, cut down on debts, and choose a lender who fits your profile. Do all this, and you won’t just get approved - you'll get a deal that works in your favor.

Ready to apply? Start fine-tuning your finances today, and make that dream home a reality!

Frequently Asked Questions:

1. What is the minimum CIBIL score required for a home loan?

Most lenders prefer a CIBIL score of 750 or above for smooth approval. A lower score may still qualify, but it could come with higher interest rates or stricter conditions.

2. How can I improve my chances of getting a higher home loan amount?

You can increase your loan eligibility by:

-

Increasing your income sources (side hustles, rental income, etc.).

-

Applying for a joint home loan with a spouse or co-borrower.

-

Making a higher down payment to lower the loan-to-value (LTV) ratio.

3. What is the ideal debt-to-income (DTI) ratio for home loan approval?

Lenders prefer a DTI ratio below 40%. This means your total monthly loan repayments (including the new home loan) shouldn’t exceed 40% of your monthly income.

4. Does changing jobs frequently affect my home loan eligibility?

Yes. Job stability matters to lenders. A steady employment history of at least 2-3 years in the same industry improves your chances. Frequent job changes can raise red flags.

5. How does a longer loan tenure impact my home loan eligibility?

A longer tenure (20-30 years) lowers your monthly EMI, making it easier for lenders to approve the loan. However, it also means you pay more interest over time.

6. Should I apply to multiple lenders at the same time for a home loan?

No. Each loan application triggers a hard inquiry on your credit report, which can lower your credit score. Instead, compare lenders and apply to 1-2 shortlisted options.

7. How does a larger down payment help in securing a home loan?

A higher down payment (20%-30%) reduces the loan amount you need, lowering the lender’s risk. This can result in better interest rates and higher approval chances.

8. Can I get a home loan if I am self-employed?

Yes, but the eligibility criteria differ. You'll need to show consistent income proof (IT returns, audited financials) for at least 2-3 years and maintain a good credit score.

Comments

No comments yet.

Add Your Comment

Thank you, for commenting !!

Your comment is under moderation...

Keep reading blogs