Buying Property in India as an NRI: Rules, Procedures, and Tax Savings Explained

Admin

Admin

- 13th Mar 2025

- 1202

- 0

Never miss any update

Join our WhatsApp Channel

Introduction

Thinking of buying property in India while living abroad? You're not alone! Many NRIs (Non-Resident Indians) see Indian real estate as a great investment option. Thanks to India's growing economy and better rules like RERA, buying property in India is now easier and safer than before.

This guide will help you understand everything about buying property in India as an NRI - from what you can buy and how to pay for it, to tax rules and selling tips. Whether you want to invest for profits, plan for retirement, or just have your own home in India, this guide has got you covered.

What Property Can NRIs Buy in India?

Types of Properties Available

As an NRI, you can buy these types of properties in India:

- Homes (flats, villas, houses)

- Commercial spaces (offices, shops)

- Industrial properties

But there are some limits too. Under FEMA rules, NRIs cannot buy:

- Agricultural land

- Farmhouses

- Plantation properties

These rules protect India's farming sector while still letting NRIs invest in homes and commercial buildings.

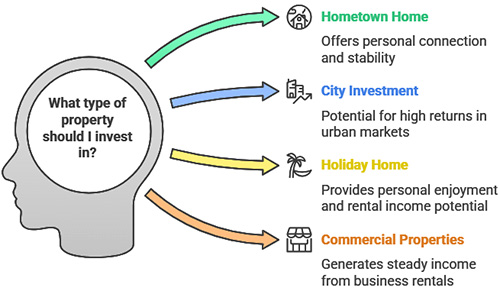

How Many Properties Can You Buy?

Good news! There's no limit on how many homes or commercial properties NRIs can buy in India. The Reserve Bank of India (RBI) doesn't restrict the number of properties you can own.

This means you can have:

- A home in your hometown

- Investment properties in big cities

- A holiday home in a tourist spot

- Shops or offices in business areas

FEMA Rules for NRI Property Purchase

The Foreign Exchange Management Act (FEMA) controls how NRIs buy property in India. Main rules include:

- How to Pay: You must pay through normal banking channels like money transfers from abroad or from your NRE/NRO accounts.

- Property Papers: All property papers must be properly signed and registered as per local laws.

- Farm Land Exceptions: While you can't directly buy farm land, you can:

- Get farm land as inheritance from resident Indians

- Ask RBI for special permission (they decide case by case)

- Change land use from agricultural to non-agricultural (with proper permits)

- Money Transfer Limits: There are some limits on sending money abroad after selling property, especially for inherited properties.

How RERA Protects NRI Buyers

The Real Estate Regulatory Authority (RERA) Act of 2016 has made buying property in India much safer. For NRIs, RERA offers these protections:

- Project Registration: All real estate projects must be registered with RERA

- Separate Bank Accounts: Builders must keep money for each project separate

- Deadline Compliance: Builders must finish projects on time

- Clear Information: All project details must be shown on the RERA website

- Penalties: Builders face fines for delays or breaking agreements

RERA works in more than 22 states and 6 union territories in India. Always check if a project has RERA registration before buying to stay protected.

Home Loans for NRIs

Who Can Get an NRI Home Loan?

Banks in India offer special home loans for NRIs. You usually need:

- Age: 21-65 years

- Job stability: At least 2 years of work experience

- Good credit score

- The loan can cover up to 80% of property value

- The property must be approved by the bank

Papers You Need

Common documents for NRI home loans include:

- Passport and visa copies

- Proof that you're an NRI

- Income proof (salary slips, bank statements, tax returns)

- Job details

- Credit history

- Property papers

Loan Repayment

NRI home loans usually run for 15-20 years, though some banks offer up to 30 years. Remember:

- EMIs must be paid from NRE/NRO accounts only

- Interest rates are a bit higher than loans for resident Indians

- Early payment options exist but might have fees

- Some banks have special deals with good interest rates for NRIs

Tax Rules for NRI Property Owners

TDS on Property Purchase

When buying property in India, NRIs need to know about Tax Deducted at Source (TDS):

- When buying from a resident Indian (property worth over ₹50 lakh): 1% TDS

- When buying from another NRI with long-term capital gains: 20% TDS

- When buying from another NRI with short-term capital gains: 30% TDS

TDS must be paid within 30 days, or you'll face penalties for late payment.

Tax Benefits for NRI Property Investors

NRIs can enjoy several tax benefits when investing in Indian property:

- Home Loan Benefits:

- Interest payment deduction up to ₹2 lakh yearly under Section 24

- Principal repayment deduction up to ₹1.5 lakh under Section 80C

- Rental Income Benefits:

- Standard deduction of 30% on yearly rental income

- Deduction of municipal taxes paid during the year

- Capital Gains Benefits:

- No tax on long-term capital gains if you reinvest in another property (Section 54)

- No tax if invested in specific bonds (Section 54EC)

- Other Benefits:

- Tax-free interest income on some government bonds

- Deduction for health insurance premiums up to ₹50,000 for seniors

Selling Property as an NRI: Rules and Steps

Who Can You Sell To?

As an NRI, you can sell your property to:

- Resident Indians without any restrictions

- Other NRIs/PIOs with RBI approval

- Foreign nationals are NOT allowed to buy from you

Papers Needed for Property Sale

To sell property in India, NRIs need:

- Property title deed

- No objection certificate (NOC) from relevant authorities

- Occupation certificate

- Plan approval certificate

- Society share certificate (for flats in buildings)

- PAN card

- NRO bank account details

If you can't visit India, you can give Power of Attorney (POA) to someone you trust who can handle the sale for you.

ALSO READ :- 10 Innovative Ideas to Tap the NRI Market for Indian Real Estate

Reducing TDS on Property Sale

NRIs can reduce the standard 20% TDS on property sale by:

- Applying for a lower deduction certificate using Form 13

- Getting the tax officer to check your actual tax amount

- Giving this certificate to the buyer before the sale

This can help you save a lot on taxes and improve cash flow from your sale.

New Trends in NRI Property Investment

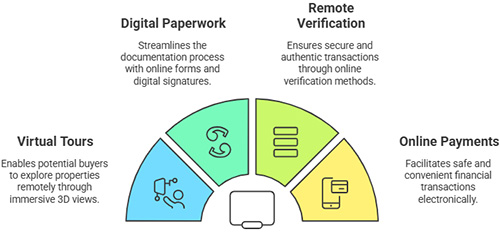

Digital Property Deals

The digital change in India's real estate makes it easier for NRIs to buy property from afar:

- Virtual property tours and 3D views

- Online paperwork and digital signatures

- Remote verification processes

- Online payment options for safe transactions

Hot Investment Spots

Beyond the big cities, NRIs are now looking at:

- Tier-2 cities with growing infrastructure

- Smart city projects backed by the government

- Township projects with better facilities

- Co-working and co-living spaces in urban areas

- Luxury holiday homes in tourist spots

Other Ways to Invest

Besides directly buying property, NRIs can now try:

- Real Estate Investment Trusts (REITs)

- Property management services for rental income

- Fractional ownership platforms

- Real estate-focused funds

Practical Tips for NRI Property Buyers

Checklist Before Buying

Before finalizing any property purchase, NRIs should:

- Check the builder's reputation and track record

- Verify RERA registration

- Review title documents carefully

- Check location potential and infrastructure development

- Understand all payment terms and hidden costs

- Talk to legal experts who know NRI property laws

- Plan how to manage the property when you're not there

- Think about long-term goals (rental income vs. value growth)

Managing Property From Abroad

For NRIs who can't visit India often, property management options include:

- Professional property management services

- Family members as caretakers with legal papers

- Tech-based security and monitoring systems

- Rental management agencies handling tenant matters

Key Points to Remember for NRI Property Investors

- Know the Legal Limits: You can buy homes and commercial properties but not farm land without special permission.

- Use Financing Options: Many home loans are available, with one loan per property.

- Use Power of Attorney: For buying from abroad, a trusted person can act for you.

- Pay All Taxes: Make sure to pay TDS, stamp duty, and other taxes.

- Rental Income: You can rent out your property, but the income is taxable in India.

- Capital Gains: When you sell property, including inherited property, you'll pay capital gains tax.

- RERA Protection: Always check for RERA registration to protect yourself.

- Use Technology: Use tech tools to manage and monitor your property from abroad.

Frequently Asked Questions

1. Can NRIs buy agricultural land in India?

No, NRIs cannot directly purchase agricultural land, farmhouses, or plantation properties in India, though they can inherit such properties from resident Indians or seek special RBI permission.

2. What are the payment methods available for NRIs to purchase property in India?

NRIs can make payments through normal banking channels, including foreign remittances or from their NRE, NRO, or FCNR accounts maintained in India.

3. Do NRIs need to be physically present in India to complete property transactions?

No, NRIs can execute a Power of Attorney to a trusted representative in India who can handle all aspects of the transaction on their behalf.

4. What is the maximum home loan amount available to NRIs?

Most financial institutions offer NRIs home loans up to 80% of the property value with loan tenures typically ranging from 15-20 years.

5. Can NRIs rent out their property in India?

Yes, NRIs can rent out their properties in India, but the rental income is taxable and must be credited to the NRI's NRO account.

6. How can NRIs repatriate funds from property sales?

NRIs can repatriate up to USD 1 million per financial year from property sale proceeds, subject to applicable taxes and obtaining a chartered accountant certificate.

7. What are the tax implications when an NRI sells property in India?

When an NRI sells property, the buyer must deduct TDS at 20% for long-term capital gains or 30% for short-term gains, though NRIs can apply for a lower TDS certificate if their actual tax liability is less.

8. How has RERA changed the property buying experience for NRIs?

RERA has enhanced transparency by requiring project registration, establishing escrow accounts, standardizing agreements, and creating a dedicated authority for addressing grievances between NRIs and developers.

ALSO READ :- The Ultimate Guide On Ghar to Building Profitable Subscription Models for Real Estate Platforms

Comments

No comments yet.

Add Your Comment

Thank you, for commenting !!

Your comment is under moderation...

Keep reading blogs