Tax Benefits of Under-Construction Properties: Maximize Your Savings

Admin

Admin

- 8th Mar 2025

- 1194

- 0

Never miss any update

Join our WhatsApp Channel

Buying a home ranks among life's biggest money decisions. While ready homes let you move in right away, under-construction properties offer some sweet financial perks - especially when it comes to tax savings.

Why Under-Construction Properties Make Financial Sense

Looking for a bargain? Under-construction homes typically cost 15-20% less than ready-to-move options. This upfront saving is just the beginning! These properties also come with tax advantages that can lighten your financial load over the years.

For people with regular salaries who need home loans, these tax benefits become particularly valuable once you get your keys. India's Income Tax Act 1961 includes special sections - 24B, 80C, 80EE, and 80EEA - designed to make buying a home more affordable through clever tax deductions.

Section 24B: The Big Interest Saver

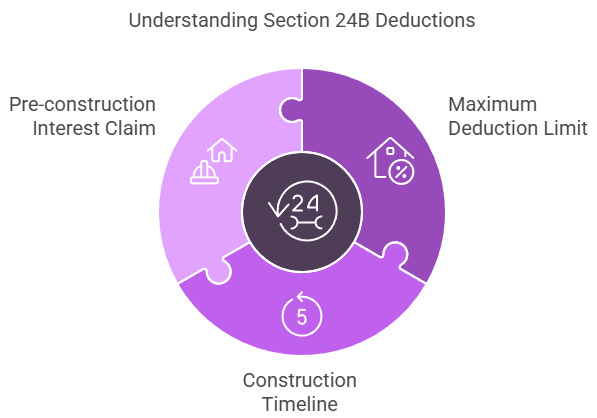

Got your eyes on Section 24B? This provision offers one of the biggest tax breaks. After your building is finished and you've taken possession, you can claim up to ₹2 lakh off your taxes each year for the interest paid on your home loan.

Remember - you can't claim this while construction is still happening. It only kicks in after completion when you physically possess the property. This ₹2 lakh limit covers both current-year interest and one-fifth of what you paid during construction.

Many buyers choose to pay just the interest portion during construction, putting off full EMIs until they take possession. Starting regular EMIs early to shorten your loan? Keep in mind that principal payments made during construction won't qualify for deductions.

How to Calculate Your Pre-Construction Period for Maximum Benefits

Want to get the most tax benefits under Section 24B? You'll need to figure out your pre-construction period correctly:

- Mark down when your home loan was approved

- Note when you started making EMI payments

- Record when construction finished and you got possession

- Identify the last day of the financial year just before you got the property

- The time between loan approval and construction completion is your pre-construction period

You can claim the total interest paid during this pre-construction period as a tax benefit under Section 24B. But here's the trick - divide this amount into five equal parts, claiming one part each year for five years. This smart approach helps you maximize deductions while staying within yearly limits.

Important Things to Remember About Section 24B

When claiming these benefits, keep these points in mind:

- Your ₹2 lakh maximum deduction includes both this year's interest and your chunk of pre-construction interest

- Construction must finish within five years from when you borrowed the loan

- If your loan started and EMIs began in the same financial year, you can claim all pre-construction interest at once instead of spreading it out

Using Section 80C for Principal Repayments

Once construction wraps up, Section 80C comes into play. This lets you deduct up to ₹1.5 lakh each year for principal repayments. This benefit works alongside the interest deductions from Section 24B, creating a powerful tax-saving strategy.

But watch out! If you sell within five years of taking possession, these tax benefits get reversed. Tax authorities see this as an early sale that goes against why these deductions exist in the first place.

Unlike interest deductions that you can spread across years, you must claim principal repayment deductions under Section 80C in the same year you made the payments.

Extra Benefits from Sections 80EE and 80EEA

Maxed out your ₹2 lakh limit under Section 24B? Section 80EE offers an extra ₹50,000 deduction each year on home loan interest if:

- You took the loan between 2013-14 and 2016-17

- This is your first property purchase

- The property costs less than ₹50 lakhs

- Your loan amount is under ₹35 lakhs

- The loan comes from a registered financial institution

Similarly, Section 80EEA gives an additional ₹1.5 lakh yearly deduction on home loan interest after using up the ₹1.5 lakh limit under Section 80C. This works when:

- You got the loan between 2019-20 and 2021-22

- It's your first property purchase

- Stamp duty doesn't exceed ₹45 lakhs

- For city properties, the carpet area stays under 645 sq.ft

- For properties elsewhere, the carpet area is less than 968 sq.ft

Important note: You can't claim benefits under both Section 80EEA and Section 80EE at the same time.

How to Claim These Tax Benefits

When filing your income tax return, claim pre-construction interest under "Interest payable on borrowed capital" in ITR Forms 1, 2, 3, or 4. Make sure to keep all supporting documents up to date and accurate.

Beyond Tax Savings: Other Perks of Under-Construction Properties

Growth Potential

Properties often gain value during construction. By the time building finishes, your investment might be worth much more than what you paid.

Make It Your Own

Buying early might let you request changes to suit your taste - something rarely possible with finished properties.

Pay as They Build

Developers usually offer payment plans tied to construction milestones. This helps you manage cash flow better than paying one big amount upfront.

Lower Down Payment

The initial payment for under-construction properties is typically smaller than for ready homes, making it easier for more people to buy.

Smart Strategies to Maximize Your Benefits

Time It Right

Try to buy near the start of a financial year to maximize deductions on interest during construction.

Keep Good Records

Save all loan-related papers, including approval letters, interest certificates, and completion certificates to back up your tax claims.

Buy Together

Purchasing with your spouse? Setting up a joint loan lets both of you claim tax benefits separately, effectively doubling your deductions.

Stay Updated

Tax laws change periodically. Keeping informed helps you catch new opportunities for deductions or changes to existing benefits.

Conclusion: Making Smart Choices

Under-construction properties offer both immediate savings and long-term tax advantages. By understanding how to use Sections 24B, 80C, 80EE, and 80EEA of the Income Tax Act, you can cut your tax bill while building valuable property assets.

Remember that tax benefits are just one part of the equation. Also think about the developer's reputation, project timelines, location potential, and your financial situation before committing to an under-construction property.

With careful planning, the tax benefits from under-construction properties can make your real estate investment smarter, making homeownership more affordable and rewarding in the long run.

Tax Benefits Comparison Table

| IT Act Section | Maximum Benefit Amount | Applicable On | Key Condition |

|---|---|---|---|

| Section 24B | ₹2 lakh per year | Home loan interest | Only after possession |

| Section 80C | ₹1.5 lakh per year | Home loan principal | Can't sell within 5 years |

| Section 80EE | ₹50,000 per year | Additional home loan interest | For loans in FY 2013-17 |

| Section 80EEA | ₹1.5 lakh per year | Additional home loan interest | For loans in FY 2019-22 |

Frequently Asked Questions

Can I claim tax benefits while my property is still under construction?

No, tax benefits under Section 24B and 80C can only be claimed after you take possession of the completed property. However, the interest paid during construction can be claimed in five equal installments after possession.

What happens if construction takes more than 5 years?

If construction exceeds five years from the end of the financial year in which you took the loan, you'll lose the tax benefits under Section 24B for pre-construction interest.

Can both husband and wife claim tax benefits on a jointly owned property?

Yes, if the property is jointly owned and both have contributed to the home loan, each can claim tax deductions independently up to the specified limits.

Is there a minimum holding period to retain tax benefits?

Yes, you need to hold the property for at least 5 years from the end of the financial year in which you took possession to retain the tax benefits claimed under Section 80C.

Can I claim benefits under both Section 80EE and 80EEA?

No, you cannot claim tax benefits under both sections simultaneously. You must choose one based on your eligibility.

What documents are needed to claim these tax benefits?

You'll need your home loan sanction letter, interest certificates, possession certificate, and property registration documents when filing your income tax return.

How do I claim pre-construction interest in my tax return?

Pre-construction interest can be claimed under the "Interest payable on borrowed capital" section in ITR Forms 1, 2, 3, or 4.

Can NRIs claim tax benefits on under-construction properties in India?

Yes, NRIs can claim the same tax benefits as residents on their home loans for properties in India, subject to the same conditions and limits mentioned above.

Comments

No comments yet.

Add Your Comment

Thank you, for commenting !!

Your comment is under moderation...

Keep reading blogs